Insights

Technology-Led Testing Is Crucial for Modern Credit Policies

Discover why technology-led A/B testing is essential for evolving credit policies. Reduce risk, improve performance, and scale lending confidently using data-driven strategy validation.

If you plan to grow lending volumes, how certain are you that your current credit policy can scale without compromising risk?

Application volumes fluctuate throughout the year due to seasonal demand, economic shifts, and changes in consumer behaviour, and yet lenders are still expected to make swift, accurate decisions. These shifts in demand can expose cracks in existing credit strategy and highlight where rules or models may need adjusting.

Ensure your credit strategy stays aligned

Credit risk managers who have tried to push through changes in a hard-coded or traditional paper-based setup know how difficult and time-consuming it can be, as it often results in operational inefficiencies and increased risk during the implementation process:

- Operational bottlenecks - slow change cycles because of development queues and dependency on underwriter or IT resource.

- Portfolio shock - a sudden spike in default rates or unwanted risk exposure when new policies are pushed straight to the full applicant population.

- Strategy blind spots - no real-time visibility between champion and challenger logic, leaving lenders unsure whether alternative decision paths might have performed better.

Taking the time to review and A/B test your approach helps ensure operational performance remains strong, risk stays controlled, and decisioning strategy keeps pace with market dynamics. Working with a specialist technology partner ensures testing is grounded in robust data and sound methodological practice, delivering:

- Scalable testing - enabling large volumes of historical decisions to be replayed in controlled conditions to identify issues early, validate improvements, and proceed with confidence.

- Deeper performance insights - through analysis at rule, scorecard, and decision level, enabling a clearer understanding of consumer behaviour and overall performance dynamics.

- Full governance and auditability - with permission-based access, real-time visibility of active and completed A/B tests, call-level inspection, and exportable summaries for clear traceability.

For instance, a lender considering expanding approvals for near-prime applicants can test the revised model against 10,000 historic applications to see precisely how default rates, average loan value, and customer lifetime value would have shifted.

Test at scale, deploy with confidence

LendingMetrics can accelerate the development and analysis of your credit decisioning policies and scorecards with two powerful self-serve features within our Auto Decision Platform (ADP):

- ADP Passive Engines – run revised decisioning logic in parallel with the active decision engine to observe differences in performance in real time, or alternatively,

- ADP Replay Module – ‘replays’ historical data with updated logic to clearly show how outcomes would have differed.

Both facilities provide controlled, non-live testing conditions, that give lenders confidence before moving to production. This enables evidence-based adjustments, highlights potential sensitivities and operational friction points, and avoids reliance on assumptions or trial-and-error.

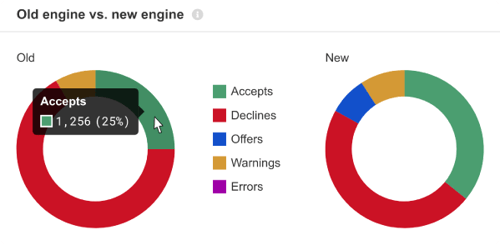

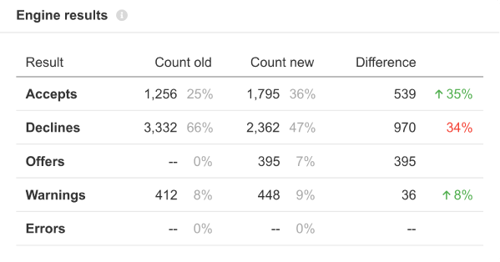

Visualise the policy changes

Within ADP, you can gain an immediate, at-a-glance understanding of how outcomes differ under the reviewed decision engine, and clearly communicate the impact of expected versus actual results.

Follow the data trail

Take it a step further by revealing the granular logic and outputs behind each decision, enabling deeper insight into performance drivers. In-depth data can also be exported to CSV for call-by-call comparison and more thorough analysis. This approach supports internal governance expectations and provides a clear, auditable rationale for policy adjustments.

See the full picture before making a change

Seeing how different decision strategies would have performed in practice allows credit risk teams to anticipate knock-on effects not only on approval rates, but on default rates, profitability, and overall portfolio quality. This helps avoid adverse selection, removes friction for desirable customers, and highlights where logic may be overly conservative or misaligned with risk appetite.

| Ultimately, lenders gain the confidence to adapt and evolve their decisioning strategies, knowing changes are grounded in evidence rather than assumption. Be confident that your decision engine delivers fair, transparent, and compliant results from day one. Don’t leave your decisioning results to chance, get in touch today to see how we can support your lending operations. |